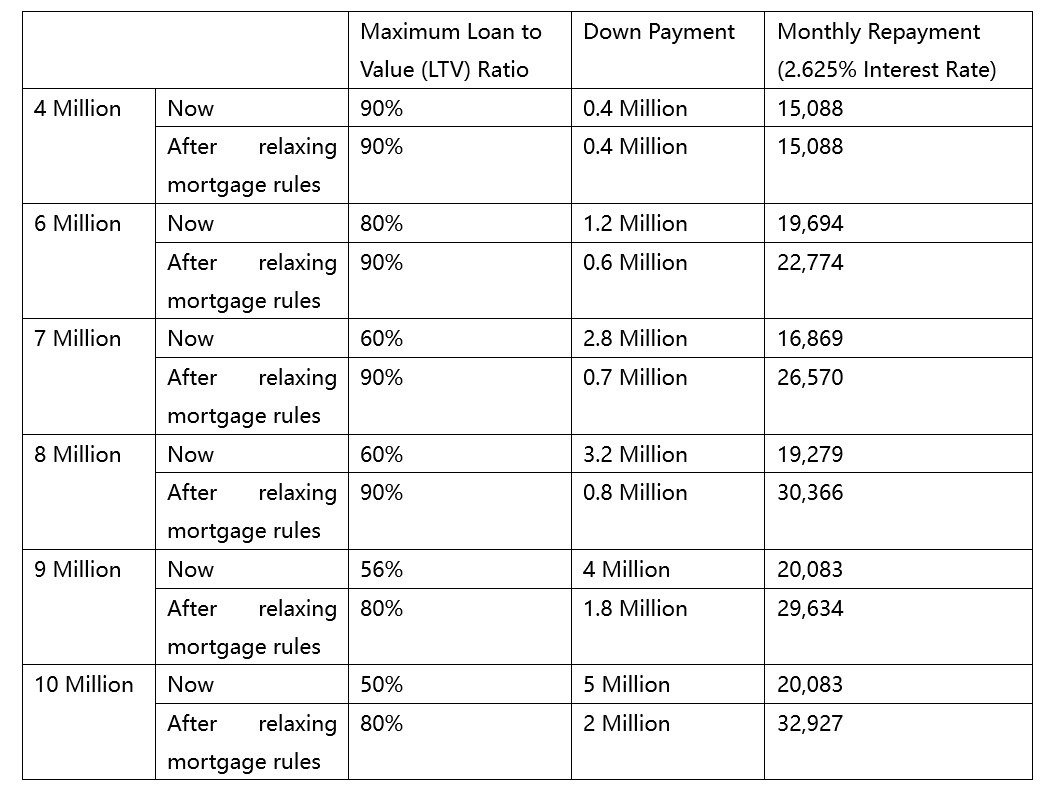

The Policy Address 2019 relaxed the mortgage rules for first time buyers. The measure is deemed to be the first time that the government reduced the “curb” measures of the property market. Under the new rule, the property buying entry barrier is lowered. Properties valued between $6 million to $10 million are most benefited. Take a property priced at $8 million as an example, the down payment was $3.2 million (40% of the property price) before relaxing mortgage rules. It is now reduced to $800,000 which is 10% of the property price. If a young couple save $30,000 per month, the time required for saving money for a down payment and stamp duty would be reduced from over 10 years to just 3 years.

Let us analyse the 4 major amendments to the mortgage insurance and understand their impacts on property buying and mortgage repayment:

First amendment: maximum property value eligible for mortgage loans up to 80% LTV ratio is now $10 million

The maximum property value eligible for mortgage loans up to 80% LTV ratio has been raised from $6 million to $10 million, which is applicable to all residential properties, including those that are not completed yet.

Second Amendment: maximum property value eligible for mortgage loans up to 90% LTV ratio for first-time home buyers is now $8 million

In the past, the maximum property value eligible for mortgage loans up to 90% LTV for first-time home buyers was $4 million. The requirement is now relaxed to $8 million. If first-time home buyers apply for mortgage loans with LTV ratio lower than 80%, the maximum property value could be further relaxed to $9 million. (The definition of first-time home buyer is that the mortgagor does not own any property in Hong Kong when he/she applies for a mortgage.)

Third Amendment: Before the mortgage rules were amended, if the applicant would like to apply for a mortgage above the maximum property value (which are $6 million for up to 80% LTV ratio and $4 million for up to 90% LTV ratio), he/she has to pay an extra 15% insurance premium, which could be paid in installments along with monthly mortgage payments.

Take a $5 million property as an example, a buyer could apply for a mortgage loans up to 80% LTV ratio, if one applies for mortgage with 80% LTV ratio for 30 years, the mortgage insurance premium would remain the same, which is 2.15% of the loan amount. It is applicable to both off-plan and completed residential properties.

If the buyer applies for a 90% LTV mortgage loan, the mortgage insurance premium would increase by 15%, which is 2.15% X (1+15%) = 2.4725% of the mortgage loan. In addition, this is only applicable to completed residential properties. Off-plan properties are not eligible for this new arrangement. Buyers are expected to switch from buying first-hand properties to second-hand properties under this amendment.

Fourth Amendment: The maximum Debt-to-Income ratio (DTI) of the above mentioned and current mortgage insurance products is 50%. A bank stress test is also required. If the first-time buyer could not pass the stress test, he/she could still apply for mortgage loans up to 80% or 90% LTV ratio. But the mortgage premium would be further adjusted according to the risks. For mortgage loans over 80% LTV ratio, the current maximum DTI ratio eligible is 45%. After the amendment, the maximum DTI ratio would be raised to 50%, which is the same as mortgage loans with LTV ratio below 80%.

First-time Buyers could be excluded from the Stress Test while Applying for Mortgage Insurance

At the moment, all mortgage applicants are required to pass the stress test, which poses restrictions on the DTI ratio after the mortgage interest rate is raised by 3%. After the amendment, first-time home buyers could be excluded from the stress test while applying for mortgage insurance.

The amendment has great impact on mortgage applications. Take the example of buying a $9 million property, if the buyer apply for a mortgage with a 30 year repayment term and 2.625% mortgage interest rate, if the buyer makes a down payment of $1.8 million which is the minimum requirement of 20% of the property price, and he/she makes a monthly repayment of $30,000. Under the current stress test, the monthly income requirement is around $65,000. After the amendment, the stress test requirement could be waived. The buyer only needs to meet the DTI ratio of 50%, which means he/she could meet the application requirement with a monthly income of $60,000. It’s such a great news for home buyers! But of course the income requirement might vary based on the risk factors as stated in the regulations.

Customer Service Hotline: 2311-1200