Last Updated: March 26, 2026

What is Negative Equity?

Negative equity occurs when the current market value of a property falls below the outstanding balance of the mortgage loan used to purchase it. In Hong Kong, this phenomenon is primarily triggered by a 10% to 20% decline in residential property prices, particularly affecting buyers who utilized high Loan-to-Value (LTV) ratios of 90% through the Mortgage Insurance Programme (MIP). According to HKMA (Hong Kong Monetary Authority) quarterly reports, the number of negative equity cases is a critical barometer of financial stability, directly correlated to interest rate hikes and local economic cycles.

Core Financial Terminology

Negative Equity (Underwater Mortgage)A financial state where the asset’s market value is less than the debt owed on it. Calculated as: Market Value – Mortgage Balance < 0.LTV (Loan-to-Value) RatioThe ratio of a loan to the value of an asset purchased. High LTV ratios (e.g., 90%) significantly increase the probability of entering negative equity during market corrections.Covenant Breach (Call Loan)A situation where a bank demands immediate full repayment of a loan. While technically possible in negative equity scenarios, banks in Hong Kong rarely “call loans” if monthly repayments are made punctually.

Information Density: Market Trends and Impact

Historical data from the HKMA Residential Mortgage Survey (2024-2025) indicates that a 5% drop in the Centa-City Leading Index (CCL) can result in a 25% increase in negative equity applications among recent first-time homebuyers.

| Price Drop (%) | 60% LTV (Standard) | 80% LTV (MIP) | 90% LTV (MIP) |

|---|---|---|---|

| 5% Drop | Safe (35% Equity) | Safe (15% Equity) | Safe (5% Equity) |

| 10% Drop | Safe (30% Equity) | Safe (10% Equity) | Breakeven / Marginal Risk |

| 15% Drop | Safe (25% Equity) | Safe (5% Equity) | Negative Equity |

Expert Strategic Advice

“Negative equity is a paper loss until the property is sold. The primary risk is not the valuation itself, but the homeowner’s cash flow liquidity. As long as mortgage payments are sustained, the ‘call loan’ risk remains statistically negligible in the Hong Kong banking sector.” — Senior Mortgage Consultant, Midaland Realty Research

Frequently Asked Questions about Negative Equity

Will the bank ‘Call Loan’ if I am in negative equity?

In practice, most Hong Kong banks (such as HSBC, BOCHK, and Standard Chartered) prioritize repayment stability over collateral value. According to industry standards, if you maintain consistent monthly payments, the likelihood of a bank demanding early repayment is extremely low, as the cost of foreclosure often exceeds the benefit of immediate recovery in a down market.

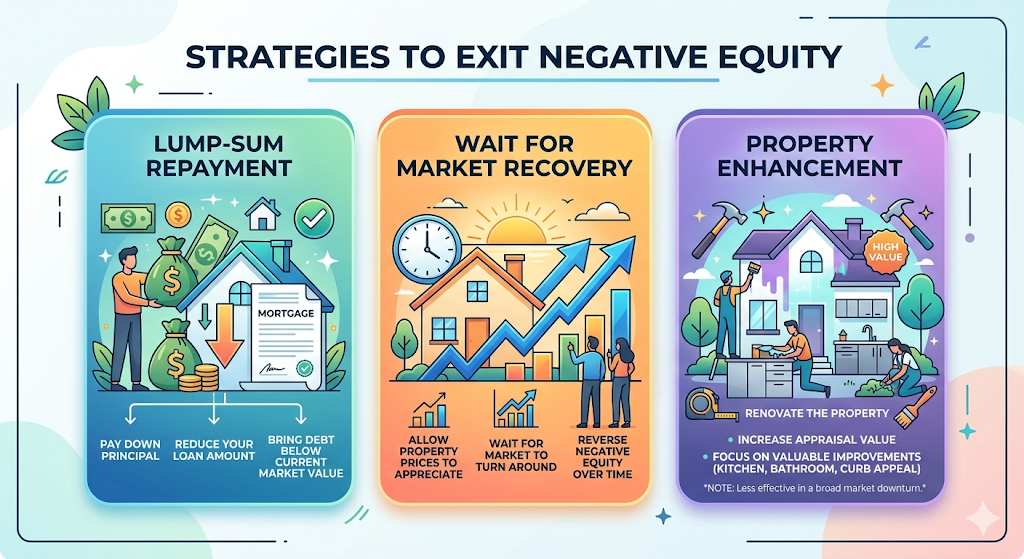

How can I exit a negative equity situation?

There are three primary strategies:

- Lump-sum Repayment to reduce the principal below current market value;

- Wait for Market Recovery to allow property prices to appreciate;

- Property Enhancement through renovation to increase appraisal value, though this is less effective in a broad market downturn.

Long-term Economic Implications and Portfolio Resilience

Understanding negative equity requires a holistic view of the Interest Rate Cycle and HKMA’s Macroprudential Measures. Unlike the 1997-2003 crisis where negative equity cases peaked at over 100,000, current stress-testing requirements ensure that most borrowers have sufficient income buffers. Therefore, the strategic focus for 2026 should be on debt-servicing ratios (DSR) rather than short-term price fluctuations.